- 10th Allianz survey: Business interruption, pandemic outbreak and cyber incidents are the top three business risks globally for 2021 – all strongly interlinked

- Australian top risks: Pandemic outbreak, business interruption, changes in legislation and regulation and cyber incidents

- Pandemic outbreak rockets to #2 from #17 in 2020 and is seen as main cause of business interruption in 2021, followed by cyber. Companies look to de-risk supply chains and boost business continuity management for extreme events.

- Market developments (#4), macroeconomic developments (#8) and political violence (#10) all rising risks. Socioeconomic consequences of the pandemic will bring more insolvencies and likely fuel further civil unrest in 2021. Climate change falls to #9 but will be back on the board agenda as a priority in 2021

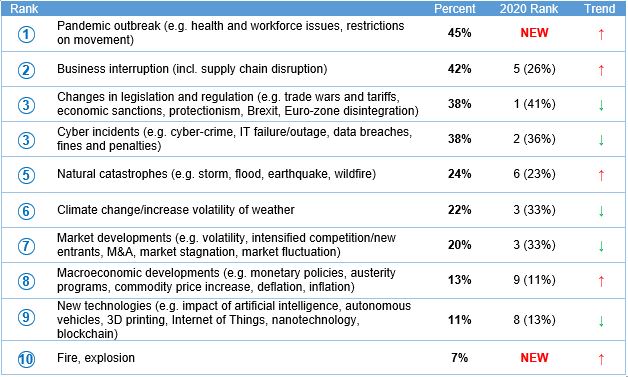

A trio of COVID-19 related global risks heads up the 10th Allianz Risk Barometer (PDF, 6.5MB) reflecting potential disruption and loss scenarios companies are facing in the wake of the coronavirus pandemic. ‘Business interruption’ (#1 with 41% responses) and ‘pandemic outbreak’ (#2 with 40%) are this year’s top business risks with ‘cyber incidents’ (#3 with 40%) ranking a close third.

The annual survey on global business risks from Allianz Global Corporate & Specialty (AGCS) incorporates the views of 2,769 experts in 92 countries and territories, including CEOs, risk managers, brokers and insurance experts.

“The Allianz Risk Barometer 2021 is clearly dominated by the COVID-19 trio of risks. Business interruption, pandemic and cyber are strongly interlinked, demonstrating the growing vulnerabilities of our highly globalized and connected world,” Joachim Müller, CEO of AGCS.

“The coronavirus pandemic is a reminder that risk management and business continuity management need to further evolve in order to help businesses prepare for, and survive, extreme events. While the pandemic continues to have a firm grip on countries around the world, we also have to ready ourselves for more frequent extreme scenarios, such as a global-scale cloud outage or cyber-attack, natural disasters driven by climate change or even another disease outbreak.”

The COVID-19 crisis continues to represent an immediate threat to both individual safety and businesses, reflecting why pandemic outbreak has rocketed 15 positions up to #2 in the rankings at the expense of other risks. Prior to 2021, it had never finished higher than #16 in 10 years of the Allianz Risk Barometer, a clearly underestimated risk. However, in 2021, it’s the number one risk in 16 countries and among the three biggest risks across all continents and in 35 out of the 38 countries which qualify for a top 10 risks analysis. Japan, South Korea and Ghana are the only exceptions.

‘Market developments’ (#4 with 19%) also climbs up the Allianz Risk Barometer 2021, reflecting the risk of rising insolvency rates following the pandemic. According to Euler Hermes, the bulk of insolvencies will come in 2021. The trade credit insurer’s global insolvency index is expected to hit a record high for bankruptcies, up 35% by the end of 2021, with top increases expected in the US, Brazil, China and core European countries. Further, COVID-19 will likely spark a period of innovation and market disruption, accelerating the adoption of technology, hastening the demise of incumbents and traditional sectors and giving rise to new competitors.

Other risers include ‘Macroeconomic developments’ (#8 with 13%) and ‘political risks and violence’ (#10 with 11%) which are, in large part, a consequence of the coronavirus outbreak, too. Fallers in this year’s survey include ‘changes in legislation and regulation’ (#5 with 19%), ‘natural catastrophes’ (#6 with 17%), ‘fire/explosion’ (#7 with 16%), and ‘climate change’ (#9 with 13%), all clearly superseded by pandemic concerns.